Over time we have written extensively about option plans, but we feel it is necessary to resume certain aspects to get a clearer picture on the matter:

- Plan construction

- Their settlement

- Their accounting

Throughout Bittnet’s history we have sought to build win-win partnerships based on the idea that you can’t build a manual of procedures and rules complex enough to eliminate undesirable behaviours, you should rather choose the right incentive systems, all parties involved will pursue the same goal without the need for controls (the “a policeman next to every citizen” approach cannot be applied because we don’t have enough cops to guard the cops). Also, it is very easy to implement the “share what we have” approach, while neither party can ‘take advantage’ of the other.

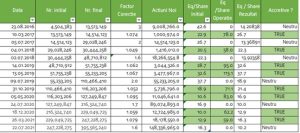

This is also how incentive plans with options are built: key people included in a plan can BUY over 2 years a number of shares representing a maximum total of 5% of the Company’s shares, at the price per share registered AT THE INCEPTION STAGE OF THE PLAN. Thus, if (and only if!) the activity of these key persons has generated an increase in the value of the shareholders’ holdings, in two years’ time, a maximum of 1/20th of this increase may be transferred to the key persons in the form of shares purchased from the company at a price equal to the historical price.

With one notable exception (Softbinator), the other listed companies have no real option plans, they offer key persons the “option” to receive a percentage of the company for free. Hence probably the confusion that “Bittnet plans are higher than the ones of other companies”, considering that in our case it is about percentage of the DIFFERENCE in capitalization, or at the other companies it is about percentage of the company.

In our case, the way we treat the team, including sharing the goodwill by means of these option plans is working as expected: Over the years, Bittnet has experienced much lower staff turnover than the companies we do business with, or the industry average, and 40% of new colleagues join the group due to referrals from other colleagues.

The settlement of these incentive plans can be made only in two ways: by repurchasing the shares of the company from the capital market in order to transfer them to the holders of options or by increasing the share capital by issuing new shares. The second option obviously dilutes the shares – those who actually approve this operation. On the other hand, it is the buyback solution that actually destroys the relevance of the SOP product by effectively decapitalising the company, because in order buy shares in the market, the company needs to pay cash which leads to decapitalisation. Moreover, at the same time, this option marks a loss of equity as the company buys “expensive” shares from the market that are at a higher price today and sells them “cheaply” at a lower price from the past. Settlement through equity increases, at the average price over the last 6-12 months or the current market price, produces value for both non-participating shareholders and key individuals: as long as the price per share is higher than the net book assets per share, non-participating shareholders increase their assets per share held:

Accounting for stock option plans is another difference between Romanian accounting standards and IFRS. If companies listed on AeRO market do not have to record any cost with the option plan, and by the time they decapitalize the company’s cash to offer free shares to employees, this is accounted for through equity and not by P&L. In other words, in RAS accounting, even if the company decapitalizes, there is no expense on the option plans.

By contrast, in IFRS accounting, even if the plans are settled through a capital increase (which in any other context is accounted for on the balance sheet and NOT in the income statement), IFRS2 requires Bittnet (and other companies in the regulated market that have or will have option plans) to account through the income statement as an expense the theoretical first issuance premium of CALL options similar to the plan approved by the General Meeting of Shareholders, REGARDLESS IF THAT PLAN EXPIRES WITHOUT BEING EXERCISED. This issue premium (calculated using the Black-Scholes formula) that the option issuer does not receive is considered ‘lost revenue’ and is written off to the P&L as a non-cash expense over the life of the plan. In other words, in the case of a properly implemented and shareholder value creating plan, although there is no cash outflow, IFRS accounting shows quarterly SOP expenses, always generating discussion among shareholders and non-shareholders, while for plans that decapitalize the company and are not real options but disguised bonuses, RAS accounting does not show any costs in the P&L at all.

We don’t intend to argue what accounting standards should look like, but we believe it is important for investors who analyze companies to understand these differences.