We are making the Bittnet Group Half Year Report – H1 2025 available to investors as a web page that is easy to follow and navigate. We are waiting for everyone’s feedback at the e-mail address investors@bittnet.ro. Thank you!

Letter from the CEO

Dear investors,

The second quarter of 2025 was strongly influenced by external factors. The presidential elections, the period of uncertainty until a new government, and discussions regarding the risk of a downgrade of the country’s rating led to a freezing period for public sector projects.

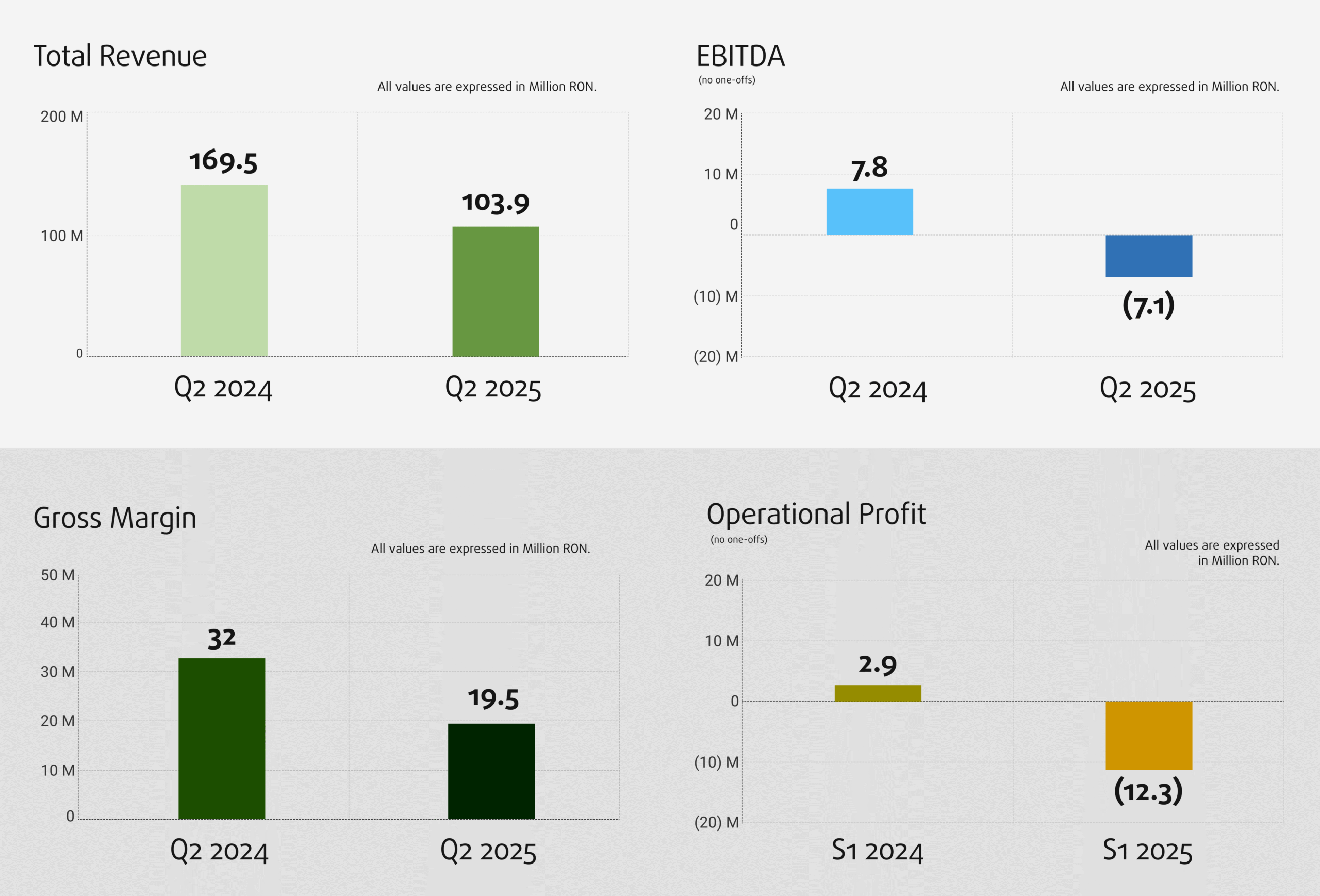

In the first half of the year, the Bittnet group recorded consolidated revenues of 103.9 million ron, -38% compared to the same period in 2024. The gross margin followed the same trend, reaching 19.5 million ron (-38% vs H1 2024), but maintaining a higher share of services in overall turnover meant that the gross margin remained at a level of 19%.

Consolidated EBITDA (excluding the provision for an litigation) was -7.1 million ron, compared to +7.8 million ron in H1 2024. Operating result was -12.3 million ron, compared to an operating profit of almost 3 million ron in the same period last year.

The financial result contributed negatively, with -4.2 million ron, composed of:

- -2.1 million ron downward revaluation of CODE stock

- -1.1 million ron losses from exchange rate differences, generated by exceeding the threshold of 5 ron for 1 euro

- partially offset by +2.8 million ron profit from the sale of the stake in Optimizor

Thus, at the level of semester 1, the group recorded a net loss of -17 million ron, compared to -4.5 million ron in the same period in 2024.

This situation was particularly felt by Dendrio, the group’s digital infrastructure pillar and one of the most important components of our business. The postponement of the signing of some won contracts, the slowdown of ongoing tenders and the delays in the collection of some invoices already issued led to an atypical 2nd quarter, with performances significantly below the historical level of this pillar, after several years in which the public sector represented a constant engine of growth and profitability for the group.

In contrast, the other pillars performed better, even if their share in total turnover is lower. In Platforms and Software pillar, Elian continued to grow, with +15% in turnover and 8 times more in operating profit. In Education pillar, we replaced large clients with a multitude of SMEs, with smaller but more diversified budgets. Starting with Q2, we delivered 64 trainings for 29 SMEs as part of the digitalization project with ADR (Romanian Digitalisation Authority) – projects worth approximately 1 million euro, ongoing and accelerating in H2. We also qualified for the final phases of a new cybersecurity training project, with an estimated value of 3 million euro.

However, the positive impact of these pillars could not compensate for the decline in the Digital infrastructure business unit, given its lower share in the group’s revenues. Historically, the second quarter had a disproportionately large contribution to results: it brought in an average of approximately 170% of Q1 in revenues and gross margin, positioning the group at or very close to profit. However, in 2025, Q2 brought in revenues similar to those of the first quarter, generated mainly by recurring contracts.

In other words, during 2020–2024, Q2 contributed an average of 27% to annual revenue and gross margin, while in 2025 its contribution was only 15% of estimated revenue for the full year.

To all these challenges, two surprising elements were added, which accentuated the negative impact of the second quarter.

The first concern, the dispute with Anchor, regarding the change of headquarters in 2020: the appeal court completely reversed the initial favorable verdict and without requesting or accepting new evidence. We filed an appeal, but prudence required us to record a provision for 4.1 million ron.

The second is related to the amount of 5 million ron approved budget by shareholders in the GMS of April 2025 for a BNET share buyback offer. This amount was correlated with the last tranche of the sale of Fort (cybersecurity pillar) to Impetum, due in June 2025. The buyer informed us that it did not have funds on time and requested rescheduling until November 2025, accompanied by additional guarantees.

In parallel, in Q2 Bittnet Group accelerated the operational efficiency program, which began in 2024. Among the measures implemented in Q2, but with impact in second part of the year, are:

- cost reduction on all lines, with an estimated impact of 10 million ron in 2025 (and 14–18 million ron in the following years)

- freezing vacant positions and restructuring some teams

- optimizing marketing budgets

- a 15% reduction in the remuneration of the Board members and 25% for the CEO, as a signal that adjustments begin at the management level

- we have also reduced the costs specific to the status of a listed company, which will lead to additional savings of approximately 700,000 ron

- elimination of non-cash expenses related to the SOP program (1 million ron)

As McKinsey’s analysis shows, in 2025 strategy is no longer just planning, but a condition for survival. And the key is fast and consistent execution. At Bittnet, this meant aligning strategic decisions with daily actions: reducing customer response times, simplifying the bidding and delivery processes, and eliminating activities that did not contribute to profitability. Consolidation is not just about numbers, but about clarity and discipline.

At the same time, we have invested in the directions that define the future. Through Nenos, our software company, we have transformed AI from an abstract concept into an applied reality: AI Agents which is already running in concrete projects, automating processes and reducing work times. It is proof that we can quickly move from idea to execution and value for customers.

Even though Q2 was marked by crises and delays, starting with the third quarter we see an unfreezing projects and budgets for technological acquisitions, both in the public and private sectors.

At this moment, the backlog of contracts with delivery dates until the end of 2025 slightly exceeds the value of 215 million ron. To this is added a pipeline of projects in various bidding and negotiation phases, with a total value of approximately 580 million ron. Part of this pipeline consists of projects financed through the PNRR, retained following renegotiations, with tenders already underway.

The current management vision is that by the end of 2025 we will be able to deliver projects worth approximately 400 million ron, with a gross margin of approximately 100 million ron. Combined with cost reductions across the board, this should lead to an estimated EBITDA of +24 million ron, a operating profit of 14 million ron and anet profit of 2 million ron – influenced by the provision (one-off event) related to the Anchor litigation.

We remain realistic and cautious, but also confident that the decisions made – even if they were difficult – put us in a healthier position to build for the long term.

As always, we encourage you to send us feedback about this report, the progress of the group’s activities or our future plans. You can always contact us at investors@bittnet.ro. Investors’ opinion is always important to us.

Mihai Logofătu,

CEO & Co-founder Bittnet Group